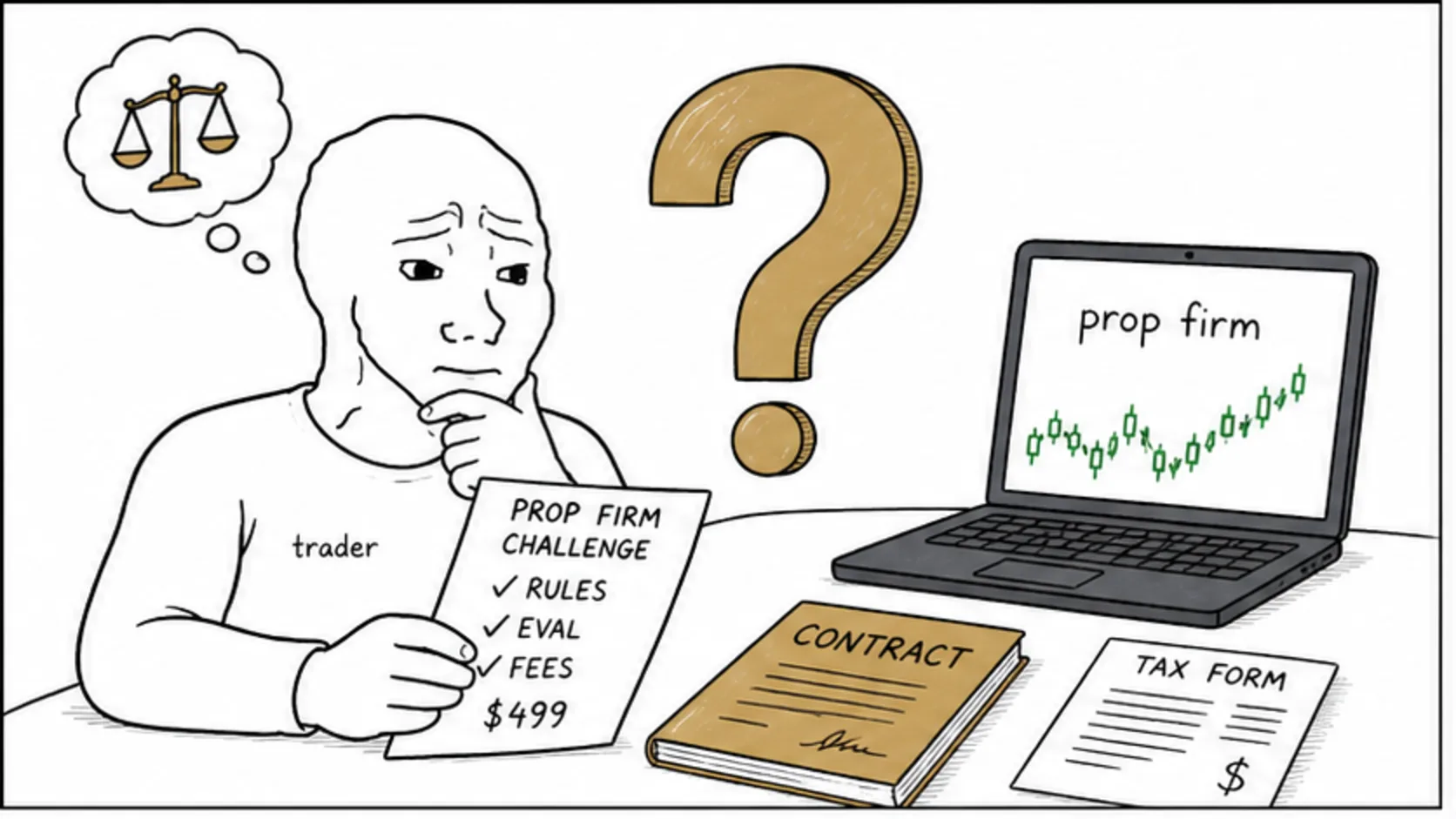

Is prop firm trading legal? Short answer: yes, in almost every country on earth. Long answer: yes, but you are participating in an almost entirely unregulated industry where your legal protections are basically whatever the firm's terms and conditions say they are. And those terms are written to protect the firm, not you. So yes, it is legal. No, that does not mean it is safe. The difference matters.

Key Takeaways

- Prop firm trading is legal in most countries because retail prop firms operate as service-based businesses, not regulated financial institutions.

- Most retail prop firms are not regulated by financial authorities like the SEC, FCA, or ASIC because they do not hold client deposits or execute live trades.

- Trading through a prop firm is not the same as trading through a regulated broker. You have fewer legal protections and no access to compensation schemes.

- The main legal risk for traders is not that prop trading is illegal, but that you have limited recourse if a firm refuses to pay you or changes its rules.

- Prop firm payouts are taxable income. You are responsible for declaring them according to your local tax laws.

On This Page

- Why the Legal Question Matters More Than You Think

- What Retail Prop Firms Actually Are From a Legal Standpoint

- The Regulatory Gap: Why Most Prop Firms Are Unregulated

- Is Prop Trading Legal in the US?

- Is Prop Trading Legal in the UK?

- Is Prop Trading Legal in Australia?

- Is Prop Trading Legal in Other Countries?

- What Legal Protections Do You Actually Have?

- Tax Implications of Prop Firm Payouts

- The Real Legal Risks for Traders

- Frequently Asked Questions

Why the Legal Question Matters More Than You Think

Most traders ask "is prop firm trading legal?" once, get told yes, and move on. That is a mistake. The question you should be asking is "what legal protections do I have if something goes wrong?" Because the answer to that one is very different from the first answer.

When you trade through a regulated broker, you have a safety net. Deposit insurance. Compensation schemes. Regulatory arbitration. Ombudsman services. Requirements for the broker to segregate your funds from their operating capital. These things exist because financial regulators spent decades building a framework to protect retail traders from exactly the kind of disaster that could wipe them out.

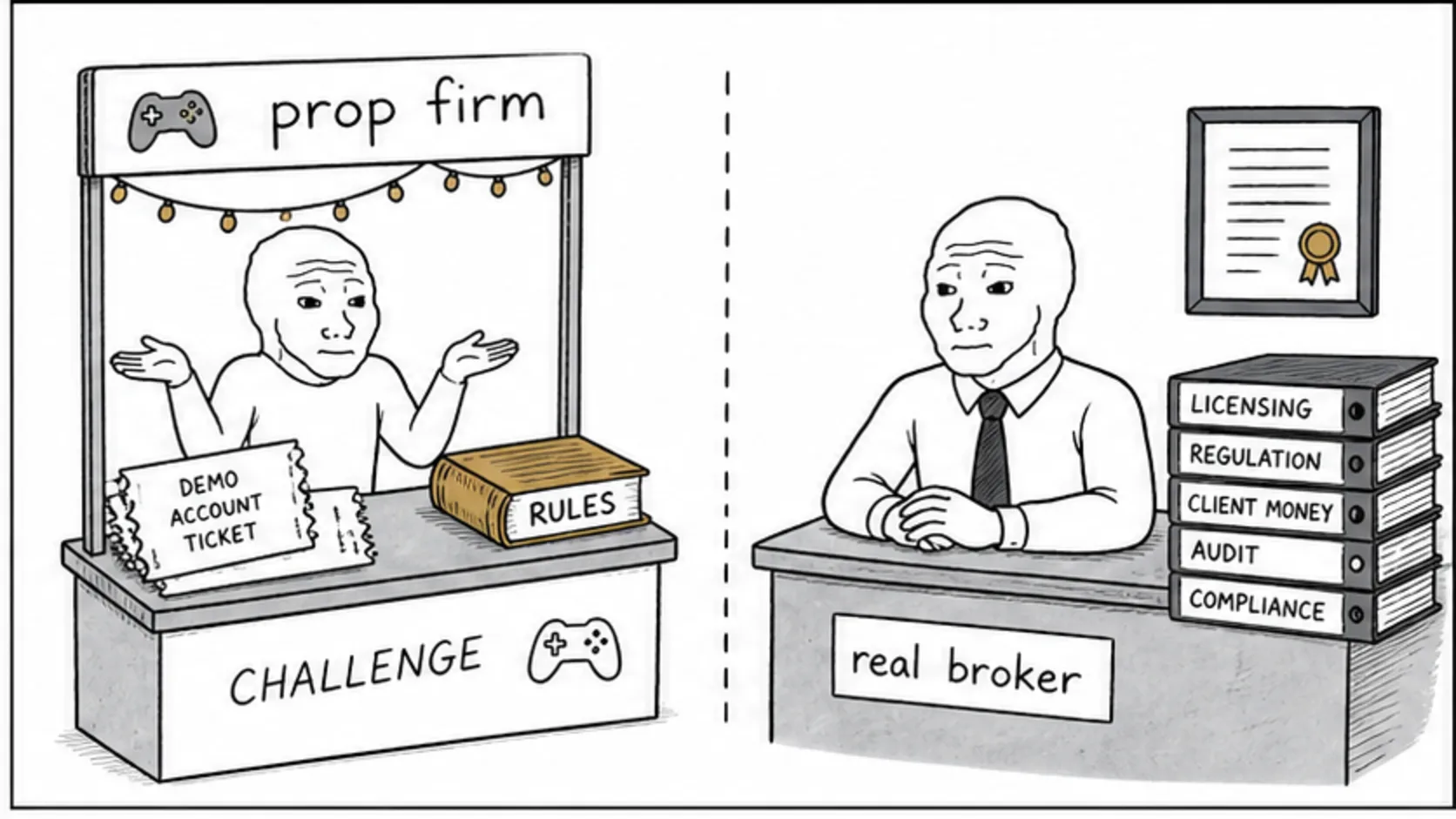

When you trade through a prop firm, most of those protections disappear. You are not a client depositing funds into a trading account. You are a customer buying a service. That service happens to involve simulated trading, but legally, you are closer to someone buying a gym membership than someone opening a brokerage account.

This distinction is the entire ball game. Prop firm trading is legal because the activity itself is legal. But the framework around it, the consumer protections, the dispute resolution, the regulatory oversight, is paper thin compared to what you get with a regulated broker.

What Retail Prop Firms Actually Are From a Legal Standpoint

Here is what most people get wrong about the legal status of prop firms. They hear "proprietary trading firm" and picture Goldman Sachs's prop desk, or a hedge fund, or some institutional operation with regulators crawling all over it. That is not what retail prop firms are.

A retail prop firm is a company that sells you access to a simulated trading environment. You pay an evaluation fee. You trade on a demo account that looks and feels like a real trading account. If you meet the performance criteria within the rules, the firm pays you a share of the simulated profits you generated.

The key legal distinction: the firm is not executing your trades on live markets. It is not holding your money in a trading account. It is not acting as a broker or an investment manager. It is providing a service, and you are paying for that service.

CFD trading through prop firms adds another layer of complexity, but the fundamental structure is the same. The firm provides the platform, the rules, and the capital allocation model. You provide the trading skill and the evaluation fee.

From a legal perspective, this makes retail prop firms similar to education companies, software-as-a-service platforms, or skill-based competition providers. The regulatory burden for these types of businesses is much lower than for financial institutions.

The Regulatory Gap: Why Most Prop Firms Are Unregulated

This is the part that should make you sit up straight.

The Securities and Exchange Commission regulates securities markets in the US. The Commodity Futures Trading Commission regulates futures and derivatives. The Financial Conduct Authority does the same in the UK. These regulators exist to protect people who deposit money with financial institutions.

But retail prop firms do not take deposits in the traditional sense. They charge fees for services. And because they operate on simulated accounts rather than live markets, they fall outside the regulatory perimeter of most financial watchdogs.

The Financial Industry Regulatory Authority requires brokers to register, maintain capital reserves, and follow strict rules about how they handle client money. Prop firms do none of this because they are not brokers. They are service providers.

This regulatory gap is not a loophole that firms are exploiting. It is a genuine gap in the regulatory framework that has not caught up to the prop firm business model. Regulators around the world are aware of it. Some are starting to look at it. But as of right now, the gap exists, and you need to understand what it means for you.

What it means is this: if a regulated broker goes bust, you have avenues to recover your money. If a prop firm goes bust, you have whatever their terms and conditions say, which is usually nothing.

Is Prop Trading Legal in the US?

Yes, prop trading is legal in the United States. But there are restrictions that US traders need to understand, because they are significant.

Futures prop firms are generally accessible to US traders. Futures trading is legal and well-regulated in the US. Prop firms that offer futures evaluations, like Topstep and Apex Trader Funding, can legally accept US traders and pay them real money for their simulated trading performance. This is the most straightforward path for American traders.

Forex prop firms are more complicated. The CFTC restricts off-exchange retail forex transactions, and CFDs are largely banned for US retail traders. Some forex prop firms get around this by offering their services through offshore entities, while others use alternative platforms like DXTrade instead of MetaTrader. Are prop firms real money? Yes, the payouts are real. But the legal mechanism for getting those payouts to US forex traders can involve offshore structures that add risk.

State-level regulations can vary. Some US states have additional financial services regulations that prop firms need to navigate. This is why certain prop firms restrict traders from specific states or change their offerings depending on where you live.

The important thing to understand is that the legality is not about whether you can trade. It is about whether the firm can legally operate the specific service model they are offering in your jurisdiction. That is their problem to solve, not yours. But if they solve it badly, you are the one who loses money.

Is Prop Trading Legal in the UK?

Yes. Prop firms are legal in the UK, and the UK actually has one of the more developed prop firm markets outside the US.

The Financial Conduct Authority does not currently regulate retail prop firms in the same way it regulates brokers and investment managers. As long as the firm is not holding client money for investment purposes, managing investments on behalf of clients, or providing regulated financial advice, it does not need FCA authorisation for its core prop trading service.

Some prop firms operating in the UK have chosen to obtain FCA registration anyway, either because they also offer regulated services or because they want the credibility that comes with regulatory oversight. But this is voluntary, not mandatory for the prop firm service model.

UK traders should be aware that FCA protections like the Financial Services Compensation Scheme do not apply to prop firm activities. If the firm fails, your evaluation fee and any unpaid profits are gone.

Is Prop Trading Legal in Australia?

Yes, prop firm trading is legal in Australia. The Australian Securities and Investments Commission takes a similar stance to other major regulators: prop firms that do not hold client funds or provide financial advice generally do not need an Australian Financial Services Licence for their core operations.

Australia has become a popular base for prop firm operations because of its well-regulated financial system and relatively clear corporate governance requirements. Several well-known prop firms are either headquartered in Australia or have Australian entities in their corporate structure.

However, ASIC has been increasingly vocal about the need for consumer protections in the retail prop trading space. Australian traders should not assume that ASIC oversight extends to their prop firm activities in the same way it covers their brokerage accounts.

Is Prop Trading Legal in Other Countries?

Prop firm trading is legal in the vast majority of countries. But there are important regional variations that matter.

European Union: Prop firms operate legally across the EU. The European Securities and Markets Authority framework focuses on investment services and client money, neither of which applies to the standard retail prop firm model. Individual EU countries may have additional requirements, but the core service is legal.

Canada: Prop trading is legal in Canada, but the regulatory environment is complex because securities regulation is handled at the provincial level rather than federally. Some prop firms restrict Canadian traders or limit their offerings in certain provinces. For tax obligations, see our Canada prop firm tax guide.

India: Prop firm trading operates in a grey area in India. The Reserve Bank of India restricts retail forex trading, but many Indian traders access prop firms that offer forex evaluations through offshore platforms. The legal status of the payouts is not always clear under Indian tax and foreign exchange regulations.

South Africa: Prop firm trading is legal and growing in South Africa. The Financial Sector Conduct Authority does not currently regulate prop firm services specifically, but its general consumer protection framework applies.

Nigeria: Prop firm trading is legal in Nigeria, and the country has a growing community of prop traders. The Securities and Exchange Commission of Nigeria has not issued specific guidance on retail prop firms.

Sanctioned countries: Prop firms universally restrict traders from countries subject to international sanctions, including OFAC-sanctioned nations. This is a legal requirement driven by the firms' payment processors and banking relationships, not by the trading activity itself.

What Legal Protections Do You Actually Have?

This is the part nobody wants to hear, but you need to hear it.

When you pay for a prop firm challenge, you are entering into a contract with a company. That contract is governed by the firm's terms and conditions, which you agreed to when you checked the box during signup. That document is your primary legal protection. Not a regulator. Not a compensation scheme. Not an ombudsman. A terms and conditions page written by the firm's lawyers.

You have been pranking yourself if you think you have the same protections as a brokerage client. Here is what you do not have.

No deposit insurance. Your evaluation fee is gone the moment you pay it. There is no scheme to recover it if the firm collapses.

No regulatory arbitration. If a regulated broker wrongs you, you can appeal to FINRA, the FCA, or ASIC. If a prop firm wrongs you, your options are civil litigation in whatever jurisdiction the firm is incorporated, which is often a different country from where you live.

No compensation scheme. The Financial Services Compensation Scheme in the UK covers up to £85,000 per person for regulated financial products. It does not apply to prop firm activities. Similar schemes in other countries have the same exclusion.

No segregation of funds. Regulated brokers must keep your money separate from their operating capital. Prop firms have no such obligation. Your evaluation fee goes straight into their operating account.

What you do have is contract law. The terms and conditions form a binding contract between you and the firm. If the firm breaches that contract, you can pursue legal action. Whether that is practical or affordable depends on the jurisdiction and the amount involved.

Tax Implications of Prop Firm Payouts

Here is something that catches a lot of new prop traders off guard. Payouts from prop firms are taxable income. I am not a tax advisor, and this is not tax advice. But I can tell you the basic framework.

When you receive a payout from a prop firm, it is generally classified as self-employment income, freelance income, or contractor income, depending on your jurisdiction and how the firm structures the payment. You need to declare it and pay tax on it.

In the US, prop firm payouts are typically reported as income on your tax return. You may be able to deduct your evaluation fees and trading-related expenses, but you should consult a qualified tax professional for the specifics of your situation.

In the UK, prop firm income is subject to income tax and potentially National Insurance contributions, depending on whether you are classified as employed, self-employed, or a contractor for the purposes of the payout.

In Australia, prop firm payouts are assessable income that needs to be declared on your tax return. The Australian Taxation Office treats this type of income similarly to other freelance or contract earnings.

The firm is unlikely to withhold tax or issue a tax document in many cases. That means the responsibility for tracking, declaring, and paying tax on your prop firm earnings falls entirely on you. Ignore this at your peril. Tax authorities are getting better at tracking online income sources, and "I did not know" is not a defence.

The Real Legal Risks for Traders

The legal risk is not that prop trading will get you arrested. That is not happening. The real risks are more boring and more dangerous.

Risk one: the firm changes the rules. Most prop firms reserve the right to modify their terms and conditions at any time. If they change the payout rules, the drawdown calculation, or the profit target after you have already paid for your challenge, you are stuck with the new terms. You agreed to this when you signed up. Read the fine print.

Risk two: the firm denies your payout. Firms deny payouts for rule breaches, consistency violations, and prohibited trading patterns. Sometimes the denial is legitimate. Sometimes it is borderline. Either way, your recourse is limited to whatever dispute resolution process the firm offers in its terms, which is usually binding arbitration in the firm's home jurisdiction.

Risk three: the firm collapses. Unregulated businesses fail all the time. When a regulated broker fails, there is a process. When a prop firm fails, there is just silence. Your evaluation fee, your funded account, your unpaid profits, all gone. Knowing the warning signs of a failing firm is your best defence.

Risk four: you cannot enforce your rights affordably. Even if the firm is clearly in the wrong, taking legal action against a company incorporated in a foreign jurisdiction is expensive, slow, and impractical for most traders chasing a few thousand dollars in unpaid payouts. The legal fees would exceed the amount in dispute.

Is prop firm trading legal? Yes. Is it regulated the way you probably expect it to be? No. The gap between "legal" and "protected" is where traders get hurt. Understand the framework, read the terms, verify the firm's legitimacy before you pay, and never put in more than you can walk away from.