Are prop firms legal in Australia? Yes. Using a retail prop firm is not illegal. Buying an evaluation, trading on a funded account, and receiving payouts are all permitted activities for Australian residents. The Australian Securities and Investments Commission has not banned prop firms or restricted Australians from participating. What ASIC has not done is regulate them, which means the same consumer protection gaps that exist everywhere else also apply in Australia. Here is the full breakdown for Aussie traders.

Key Takeaways

- Prop firms are legal in Australia. No law prohibits buying evaluations or receiving payouts from prop firms.

- Most retail prop firms are not regulated by ASIC because they do not hold an Australian Financial Services Licence.

- Prop firm income is taxable. The ATO expects you to declare it, whether as personal income or capital gains.

- Most major prop firms accept Australian traders. Unlike the US, Australia has no broad restrictions.

- ASIC has issued general warnings about unlicensed financial services but has not specifically targeted retail prop firms.

On This Page

Why Prop Firms Are Legal in Australia

The legality question comes down to what prop firms actually do. They sell evaluations, which are essentially software services. You pay a fee to access a simulated trading platform that mirrors live market conditions.

If you pass the evaluation, you get access to a funded account. That account is also simulated in most cases. No real money is being traded on your behalf on any exchange or market. The firm is not holding your deposits or investing your capital.

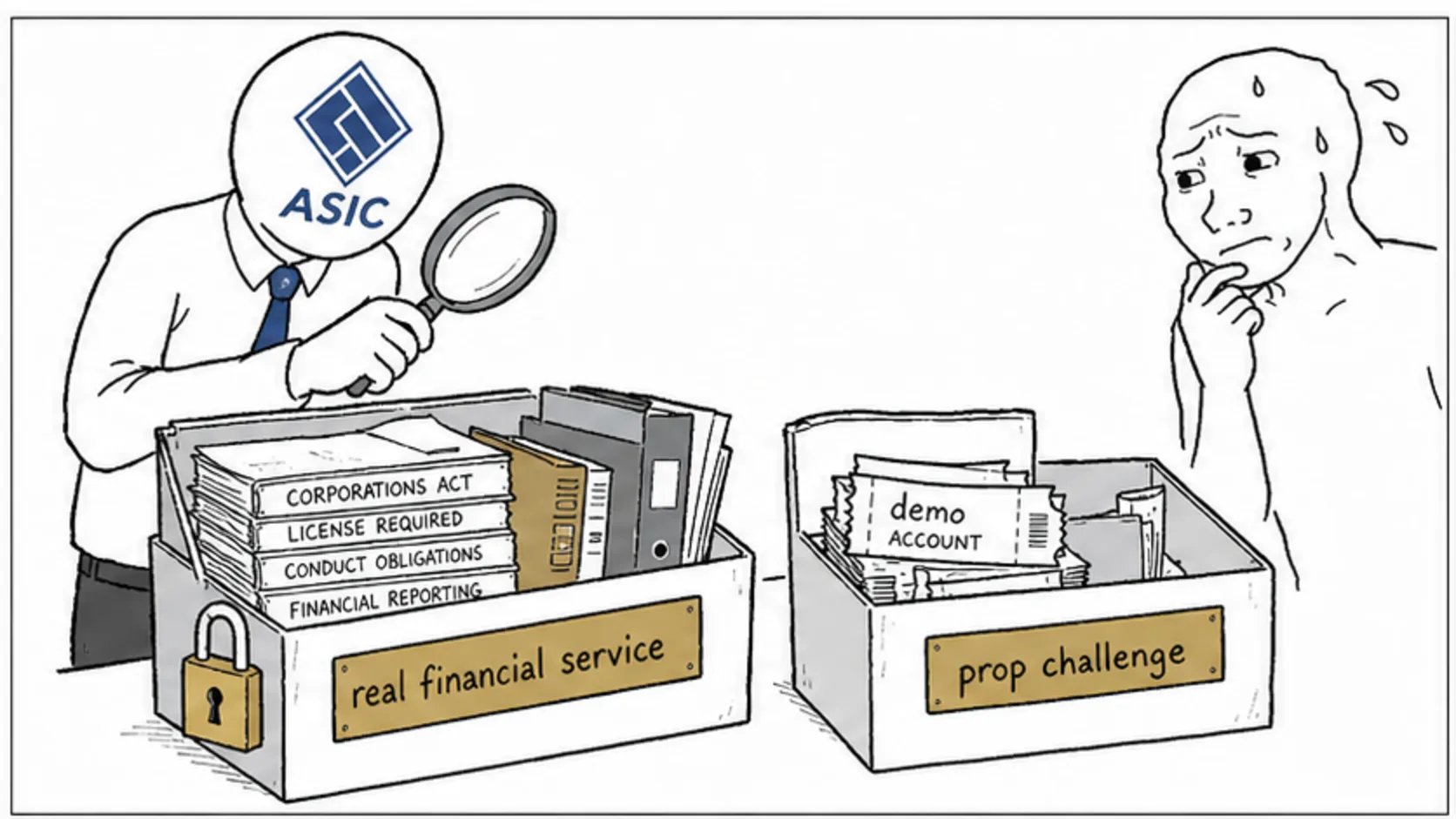

Under Australian law, this does not constitute a financial service. The Corporations Act 2001 defines financial services as dealing in financial products, providing financial product advice, or making a market. Prop firms doing none of these things sit outside ASIC's regulatory perimeter.

The prop firm business model works the same way in Australia as everywhere else. The evaluation fee is a service charge. The payout is a performance reward from the firm's own revenue. Neither of these activities requires an Australian Financial Services Licence.

This does not mean the space is completely unregulated. The Australian Consumer Law applies to the purchase of the evaluation, giving you basic protections around misleading conduct and unfair contract terms. But these are general consumer protections, not financial services regulation.

How ASIC Views Prop Firms

ASIC is Australia's corporate, markets, and financial services regulator. It oversees approximately 48,000 companies that hold Australian Financial Services Licences. Prop firms are not among them.

ASIC has issued general warnings about unlicensed financial services providers operating in Australia. These warnings are not specifically aimed at prop firms but cover any entity offering financial services without holding an AFSL.

The question ASIC has not definitively answered is whether retail prop firms are actually providing financial services. If a prop firm only offers simulated trading, the argument is that no financial service is being provided. The trader is paying for access to software, not for investment management or broker services.

This is the same regulatory grey area that exists in other jurisdictions. ASIC has not taken enforcement action against retail prop firms, unlike the CFTC in the United States. This could change if consumer harm becomes significant enough to warrant regulatory attention.

For now, ASIC's position appears to be watchful tolerance. The regulator is aware of the industry but has not determined that it falls within its regulatory scope. Australian traders should treat this as a fluid situation that could evolve.

What You Give Up Without ASIC Regulation

If a financial firm is regulated by ASIC and holds an AFSL, you get several important protections. None of these apply to your relationship with a retail prop firm.

Dispute resolution. AFSL holders must belong to an external dispute resolution scheme, currently the Australian Financial Complaints Authority. If a regulated firm treats you unfairly, you can take your complaint to AFCA, which can order the firm to pay compensation. Prop firms are not AFSL holders, so AFCA is not available to you.

Compensation. If a regulated financial firm collapses, there are compensation mechanisms available through the regulatory framework. If a prop firm collapses, your evaluation fee and any unrealised profits are gone. There is no Australian equivalent of the UK's FSCS for unregulated firms.

Capital requirements. AFSL holders must meet minimum capital adequacy requirements to ensure they can meet their obligations to clients. Prop firms have no such requirements. A prop firm could be operating with minimal financial reserves while collecting evaluation fees from thousands of traders.

This does not mean prop firms are inherently untrustworthy. It means the safety net that ASIC provides for regulated financial services does not exist for prop firm evaluations.

ATO Tax Rules for Prop Firm Income

This is where Australian traders need to pay close attention. The Australian Taxation Office considers prop firm income to be taxable, and ignoring it is a bad idea.

How your prop firm income gets taxed depends on your circumstances. If you are trading as an individual, the ATO may classify your prop firm earnings as either income from a business activity or as capital gains.

The distinction matters because the tax treatment is different. Business income is taxed at your marginal rate, which can reach 45% plus the Medicare levy for high earners. Capital gains may qualify for the 50% discount if you hold positions for more than 12 months, but most prop firm traders do not hold positions that long.

If you trade through a company structure, the company pays corporate tax at 25% on profits. You then extract money through salary, dividends, or director's fees, each with their own tax treatment.

Evaluation fees are generally deductible as a business expense, reducing your taxable income. But you need to keep proper records. The ATO can audit your returns for up to five years.

The ATO community forum has multiple threads about prop firm income, which tells you two things. First, prop firm trading is common enough in Australia that the tax office is aware of it. Second, the ATO has not provided specific guidance, which means standard tax principles apply.

Speak to a registered tax agent who understands trading income. The cost of professional advice is itself tax deductible and will almost certainly save you more than it costs.

Which Prop Firms Accept Australian Traders

Good news. Australia is one of the most accessible markets for prop firm traders. Most of the highest-rated prop firms accept Australian clients without restrictions.

FTMO, FundedNext, The5ers, FundingPips, and most other established firms process applications from Australian traders normally. The evaluation rules, profit targets, and payout processes are the same as for traders in other non-restricted countries.

The reason for this is straightforward. Australia has not experienced the kind of regulatory enforcement that hit US-facing firms. ASIC has not pressured prop firms to stop serving Australian clients, so the firms have had no reason to restrict access.

The situation is similar to the UK, where traders also enjoy broad access to most prop firms. The restrictions that exist are primarily driven by US regulators, not Australian ones.

Some smaller or newer firms may have country restrictions unrelated to regulation, often driven by payment processing limitations rather than legal concerns. Always check the firm's terms before purchasing, but Australia is rarely on any restricted list.

Australia-Specific Considerations

A few things that matter specifically for Australian traders that you will not find in generic prop firm guides.

Time zones. Australia is 8 to 11 hours ahead of London and 14 to 17 hours ahead of New York, depending on daylight saving. The London session, which handles roughly 35% of global forex turnover, starts at 5pm to 7pm AEST. The New York session starts at 10pm to midnight AEST. This means your prime trading hours are in the Australian evening and night.

Payment methods. Most prop firms accept credit cards, debit cards, and crypto. Some accept PayPal. Australian traders should check whether their bank charges international transaction fees, since most prop firms process payments in USD or EUR.

Currency conversion. Your payouts will likely be in USD. When you transfer to your Australian bank account, you will lose money on the exchange rate unless you use a service with competitive conversion rates. This is a hidden cost that many traders do not factor in.

Leverage and regulation differences. Australian forex brokers are subject to ASIC leverage limits of 30:1 for major pairs. Prop firms are not bound by these limits because they operate outside ASIC's jurisdiction. This is an advantage for traders who want higher leverage, but it also means less protection.

How to Protect Yourself as an Australian Trader

Three missions for Australian traders.

Mission one: get your tax sorted before you earn. Register for an ABN if you are trading as a business. Set up proper bookkeeping from day one. Keep records of every evaluation fee, every payout, and every trading expense. The ATO takes unreported income seriously.

Mission two: verify every firm before you buy. Check whether the firm appears on ASIC's register. If they claim to be regulated and are not on the register, walk away immediately. If they do not claim to be regulated, that is fine, but you know you have no ASIC protection.

Mission three: factor in all costs before you calculate profitability. Evaluation fees, currency conversion costs, international transaction fees, and tax obligations all eat into your returns. A $5,000 payout in USD is worth considerably less after conversion to AUD and tax.

Australia is a solid jurisdiction for prop firm traders. You have access to most firms, no regulatory barriers, and a clear path to tax compliance. The absence of ASIC regulation is a trade-off you need to accept consciously, not something to ignore and hope for the best. Get your tax right, verify your firms, and treat every evaluation fee as money you might not see again. That is the honest approach, and it works.

Australian Prop Firm Tax Obligations

Let me be blunt about this because I have seen too many Australian traders get it wrong. Prop firm income is not some grey area the ATO will overlook. It is assessable income, full stop. Here is what you need to know.

If you are trading as an individual, you need to declare your prop firm income on your tax return. The classification depends on how the ATO views your activity. If you trade frequently with a primary intention of making profit, the ATO will likely classify it as business income or trading income, taxed at your marginal rate. If you trade less frequently and hold positions longer, it might fall under capital gains. Most prop firm traders fall into the first category because the frequency of trading and the profit motive are both clear.

Do you need an ABN? Not strictly required if you are trading as a sole trader, but it helps. An ABN makes it easier to claim deductions, open a business bank account, and demonstrate to the ATO that you are running a legitimate trading activity rather than gambling. I registered for an ABN in my second year of prop trading and it simplified everything.

What can you deduct? Evaluation fees, reset fees, charting software subscriptions, trading courses, internet costs (proportionally), home office expenses if you have a dedicated trading setup, and any other expenses directly related to your trading activity. Keep receipts for everything. The ATO can audit you for up to five years, and "I think I spent about $400 on evaluations" is not going to cut it.

Currency conversion is a hidden tax trap. Your payouts arrive in USD, but you report income in AUD. The exchange rate on the day you receive the funds determines the AUD amount you declare. If the AUD weakens between when you earn and when you report, your tax bill goes up in AUD terms even though your USD income stayed the same. Track the exchange rate on every payout date.

If you are earning serious money from prop trading, consider trading through a company structure. The corporate tax rate is 25%, which can be significantly lower than the top marginal rate of 45% plus Medicare levy. Speak to a tax agent who works with traders. The advice pays for itself quickly.

Which Prop Firms Accept Australian Traders

The good news for Australian traders is that almost every major prop firm welcomes you with open arms. The regulatory pressure that has made life difficult for US traders simply does not exist in Australia, and ASIC has not taken any enforcement action against prop firms serving Australian clients.

FTMO, FundedNext, The5ers, FundingPips, and most other established firms process Australian applications without any restrictions. The evaluation rules, profit targets, and payout processes are identical to what traders in Europe and Asia experience. You are not a second class customer.

There are a few practical considerations. Payment processing is the main one. Most firms charge in USD or EUR, so your Australian bank may charge international transaction fees on top of the evaluation price. Check with your bank before buying, or use a card that waives foreign transaction fees.

Payout methods vary by firm. Some pay via bank transfer, which means currency conversion at your bank's rate. Others offer crypto payouts, which can be faster and cheaper if you are set up to receive them. A few firms support PayPal, which has its own conversion rates that are rarely competitive.

The time zone situation is worth planning around. The London forex session opens at 5pm to 7pm AEST, and the New York session starts around 10pm to midnight. If you are trading forex through a prop firm, your best trading windows are in the Australian evening and night. Futures traders have more flexibility because the CME Globex session runs nearly 24 hours.