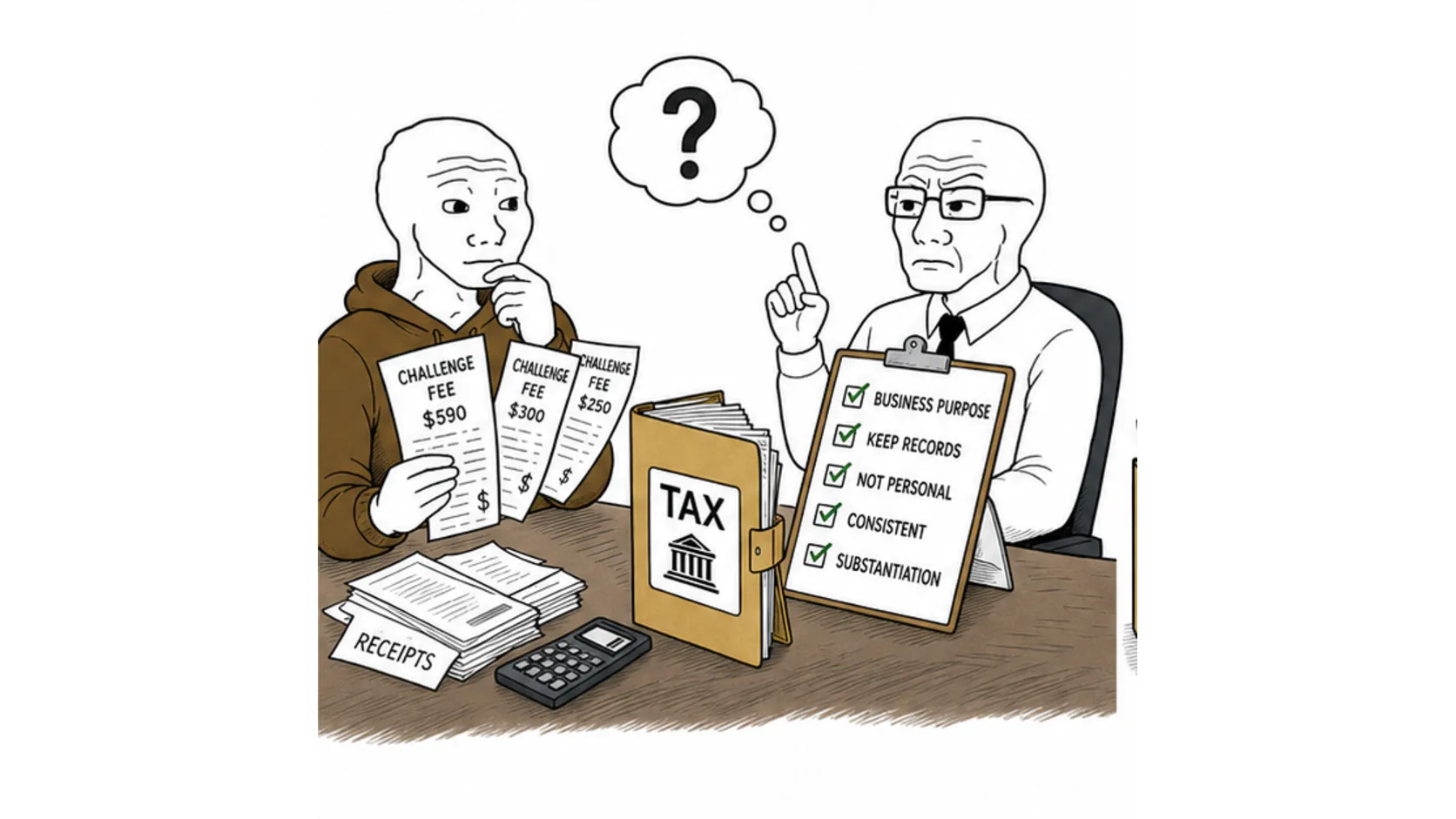

You paid $500 for a prop firm challenge, failed it, bought another one for $300, passed that one, then paid for a data feed and a VPN. Now tax season is here and you are wondering if any of that is deductible. The short answer is maybe, and the long answer depends on your country, your tax status, and whether the tax authority considers your trading a business or a hobby. This is not tax advice, but it is the framework you need to have an intelligent conversation with an accountant who actually understands prop trading.

Key Takeaways

- Prop firm challenge fees may be deductible as business expenses if you treat trading as a business, not a hobby.

- US traders can potentially deduct evaluation fees, data subscriptions, and trading software under Schedule C.

- UK traders report prop firm income as self-employment income and can claim allowable expenses against it.

- You cannot deduct fees against prop firm payouts that are classified as independent contractor income in all cases. It depends on your tax status.

- Always consult a tax professional who understands trading income. General tax advice does not cover prop firms well.

The Short Answer on Prop Firm Fee Deductions

Prop firm fees can be tax deductible, but only if your tax authority classifies your trading as a business activity rather than a hobby. In the US, this means you need to qualify as a "trader" under IRS rules, which is harder than it sounds. In the UK, it means registering for self-assessment and declaring your trading income as self-employment.

The distinction between business and hobby is the entire ballgame. If the IRS or HMRC decides you are a hobby trader, your deductions are limited or nonexistent. If they classify you as a business, a whole range of expenses become deductible.

Here is the problem with prop firms specifically. You are not trading your own money. You are paying fees to access someone else's capital, and the payouts you receive are often classified as independent contractor income, not investment gains. That classification changes how your fees interact with your tax return.

Are Prop Firm Challenge Fees Tax Deductible?

Challenge fees, evaluation fees, and reset fees are the most common expenses prop traders want to write off. Here is how they work in practice.

Passed the challenge and got funded. The fee you paid to take the challenge is likely deductible as a business expense. It was a cost incurred to generate income (your funded account payouts). This is the cleanest scenario for deduction.

Failed the challenge and never got funded. This is where it gets murky. If you are a business trader, failed challenge fees can potentially be deducted as a business loss or expense. If you are a hobby trader, you generally cannot deduct them. The IRS discontinued miscellaneous deductions for hobby expenses under the Tax Cuts and Jobs Act of 2017.

Bought multiple challenges in one year. If you spent $2,000 on challenge fees across 5 different firms and only passed one, the $2,000 total may be deductible if you qualify as a business trader. You would report this on Schedule C as a business expense.

The key factor the IRS looks at is whether you are trading with "continuity and regularity" and whether you are trying to make a profit. If you bought one challenge, failed it, and never tried again, that looks like a hobby. If you are consistently trading, buying evaluations, and treating this as a business, you have a stronger case.

Data Feeds, Software, and Other Deductible Expenses

If you qualify as a business trader, these expenses are generally deductible:

- Trading platform fees (NinjaTrader license, TradingView Pro, etc.)

- Data feed subscriptions (CME real-time data, Level 2 data)

- VPS hosting if you run EAs or automated strategies

- Trading education (courses, books, coaching) if directly related to your trading business

- Internet and phone (partial deduction for business use)

- Home office (if you have a dedicated trading space)

- Computer equipment (monitors, laptops) used for trading

The list is similar to what any self-employed person can claim. The difference is that traders often overlook some of these because they do not think of themselves as running a business.

Here is the catch. You can only deduct expenses up to the amount of income you generate. If your prop firm payouts total $5,000 for the year and your expenses are $8,000, you cannot create a $3,000 tax loss from a hobby classification. Under business classification, you may be able to carry the loss forward or offset other income, depending on your exact situation.

How US Traders Handle Prop Firm Taxes

For US-based traders, prop firm income is usually reported as ordinary income, not capital gains. This is because you are not investing your own capital. You are receiving payments from the prop firm based on your trading performance.

Most prop firms issue a 1099-NEC (non-employee compensation) to US traders who receive payouts. This goes on Schedule C as self-employment income. You also owe self-employment tax (15.3%) on top of regular income tax.

That sounds bad, and it is. But the flip side is that Schedule C allows you to deduct business expenses against that income. Your challenge fees, data feeds, software, and other trading costs all reduce your taxable income dollar for dollar.

The self-employment tax is the part that catches people off guard. A $10,000 prop firm payout does not mean $10,000 in your pocket. After self-employment tax and income tax, you might keep $6,500 to $7,500 depending on your tax bracket. Plan for this.

If you qualify as a "trader in securities" under IRS guidelines (which requires significant trading activity on your own accounts), you might be able to use mark-to-market accounting. But prop firm trading alone usually does not qualify you for this status, since you are not trading your own securities.

How UK Traders Handle Prop Firm Taxes

UK traders face a different but equally confusing system. Prop firm payouts in the UK are generally treated as income, not capital gains, because you are not investing your own money.

If you are trading through a prop firm as an individual, you register for self-assessment with HM Revenue and Customs and report your prop firm income as self-employment income. You can then claim allowable expenses against this income.

Allowable expenses for UK prop traders include challenge fees, platform subscriptions, data feeds, training courses, and a portion of your internet and home office costs. The rules are similar to the US in principle, though the specifics differ.

The trading allowance in the UK lets you earn up to £1,000 from self-employment without declaring it. If your prop firm income is below this threshold, you do not need to report it. If it is above, you report the full amount but can choose between claiming the £1,000 trading allowance or deducting actual expenses.

For most funded traders making regular payouts, deducting actual expenses is better than taking the £1,000 allowance, because your total expenses likely exceed £1,000 when you include challenge fees and software.

What You Cannot Deduct

Not everything is deductible, and claiming deductions you are not entitled to is how traders get audited. Here is what you generally cannot write off.

Personal losses from your own trading accounts. If you have a personal forex or futures account and lose money trading it, those losses may be deductible separately. But they do not offset prop firm income directly unless you qualify for specific trader tax status.

Time spent trading. You cannot deduct your time. If you spend 6 hours a day trading on a funded account, that labor cost is not deductible. Self-employed people often forget this.

General financial education. A book about personal finance is not deductible. A course specifically about prop firm trading strategies probably is. The distinction matters.

Expenses from before you started trading as a business. If you bought a laptop two years before you ever heard of prop firms, you cannot retroactively claim it as a business expense. The expense needs to be incurred during the period you were actively trading as a business.

Fines and penalties. If a prop firm charges you a reset fee because you breached a rule, that is arguably a cost of doing business. But if it is characterized as a penalty, some tax authorities may not allow it. This is a gray area.

Record Keeping for Prop Traders

If you want to deduct prop firm fees, you need documentation. Not "I think I paid about $500 to some firm in March." Actual records.

Here is what you should keep for every tax year:

- Challenge fee receipts from every prop firm you paid, whether you passed or failed

- Payout confirmations showing the gross amount received from each firm

- 1099-NEC forms (US) or equivalent income documentation

- Software and data subscription receipts

- VPS hosting invoices

- Bank statements showing prop firm deposits and withdrawals

- A trading log showing dates, times, and results (supports your claim of business activity)

Keep these records for at least 3 years (US) or 5 years (UK) after filing. The IRS can audit returns up to 3 years back, longer if they suspect underreporting.

Getting It Right at Tax Time

The problem with prop firm taxes is that most accountants do not understand how prop firms work. They understand stocks, bonds, and maybe forex. But the idea that you pay a fee to trade someone else's money and get payouts classified as contractor income is not something most tax professionals encounter regularly.

You need an accountant who understands trader tax status, or at minimum someone willing to learn. The wrong advice can cost you thousands in missed deductions or, worse, trigger an audit because you filed incorrectly.

Three practical moves for tax time:

First, separate your prop firm finances from your personal finances. Open a dedicated bank account for prop firm income and expenses. This makes tracking everything dramatically easier and looks better if you are ever audited.

Second, track your income and expenses monthly, not just at tax time. Use a spreadsheet or accounting software. Every challenge fee, every payout, every data subscription. When April comes, you just export the numbers instead of reconstructing the entire year from memory.

Third, set aside 25-30% of your prop firm payouts for taxes throughout the year. Do not wait until the tax bill arrives. If you get a $5,000 payout and spend all of it, you will owe approximately $1,250 to $1,500 in self-employment and income tax on that payout alone. Plan your tax obligations from the first payout, not the last.

Whether prop firm fees are tax deductible depends on your situation, your country, and how seriously you treat your trading. The traders who get the best tax outcomes are the ones who keep clean records, understand their classification, and work with a professional who knows the difference between a prop firm challenge and a stock trade. Sort that out early and you keep more of every payout you earn.